Noah Shurtliff

Helping Phoenix families become homeowners and build long-term wealth, Noah Shurtliff simplifies the mortgage process so clients can make confident decisions (recognized as a top-growing loan officer in 2021).

Phoenix-born and Valley-raised, he also leads The Social Entrepreneur. Ready to make your next move? Contact Noah to explore your options.

Thousands of price reductions and shifting rates have quietly created one of the best buyer’s windows in years.

By Noah Shurtliff, Mortgage Advisor, and Morgage Editor

I just got back from Los Angeles, and one conversation stuck with me the whole flight home. I was out there visiting Giovanni and his father Johnny. Two clients who’ve built a quiet, smart investment operation buying single-family homes and adding ADUs in the back. More units, more inventory, more long-term equity. It works because they understood something early: housing demand doesn’t wait for perfect conditions. You build into the need, not around it.

Standing in one of their backyards, looking at what used to be dead space and is now a livable unit generating rent, I kept thinking that’s exactly the mindset missing from conversations I’m having every day back home in Phoenix.

The opportunity here is real, and most people are standing in their own way. Arizona is in a buyer’s market. Sit with that for a second, because it hasn’t been true in a long time.

Thousands of price reductions are hitting the Phoenix MLS right now. Sellers who held firm for years are adjusting. Buyers who show up with a clear strategy have more leverage than they’ve had in years. Rates ticked up through March, then started coming back down in April, and that small shift alone was enough to bring buyers back off the sidelines.

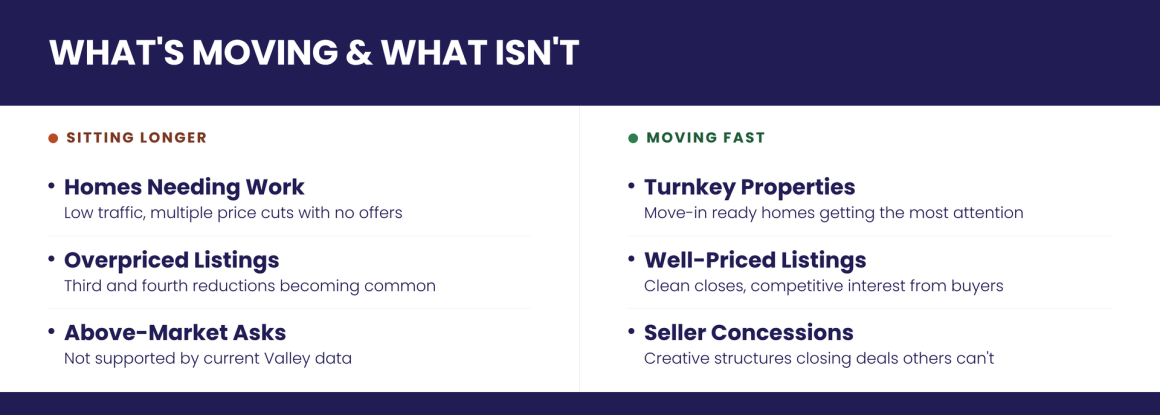

Inside that broad picture, a split is forming that tells you where the real opportunity lives. Turnkey homes move-in ready, clean, well-priced — are moving quickly. Homes that need work or came in above what the data supports are sitting, some through their third or fourth price reduction. The gap between those two categories is widening every week. If you know which side of that line to be on, this market is working in your favor.

A client of mine named George came to me stuck. He’d refinanced during COVID when rates were in the low 3s, and that number had become his anchor the payment he measured everything else against. When he decided to sell and move into a new home in Gilbert, the rate gap between then and now felt like a wall. He almost didn’t move forward. We sat down and I asked him one question: What monthly payment would let you sleep at night?

Not what rate. Not what the market was doing. Not what his neighbor paid in 2021. What number works for your life right now? We built everything backwards from there. Found a loan structure that hit that number.

Ran the long-term math on equity growth and what a future refinance looks like when rates come down. Showed him that the cost of waiting another year out of the market was higher than the cost of a rate he didn’t love. George closed last month. He’s in Gilbert, building equity, and he’s set up to refinance when the time is right.

The rate isn’t what he paid in 2021. But he’s in the market, which is the only place any of this actually compounds. Most people think waiting is the safe move. It isn’t. I’ll buy when rates drop. When prices fall. When inflation cools. When the economy feels more stable.

Some version of that is the most common thing I hear. I understand it; the headlines make buying feel impossible right now. But waiting has a cost that doesn’t show up on any spreadsheet. It shows up in the equity you didn’t build, the seller concessions you didn’t capture, the price reductions you watched someone else take.

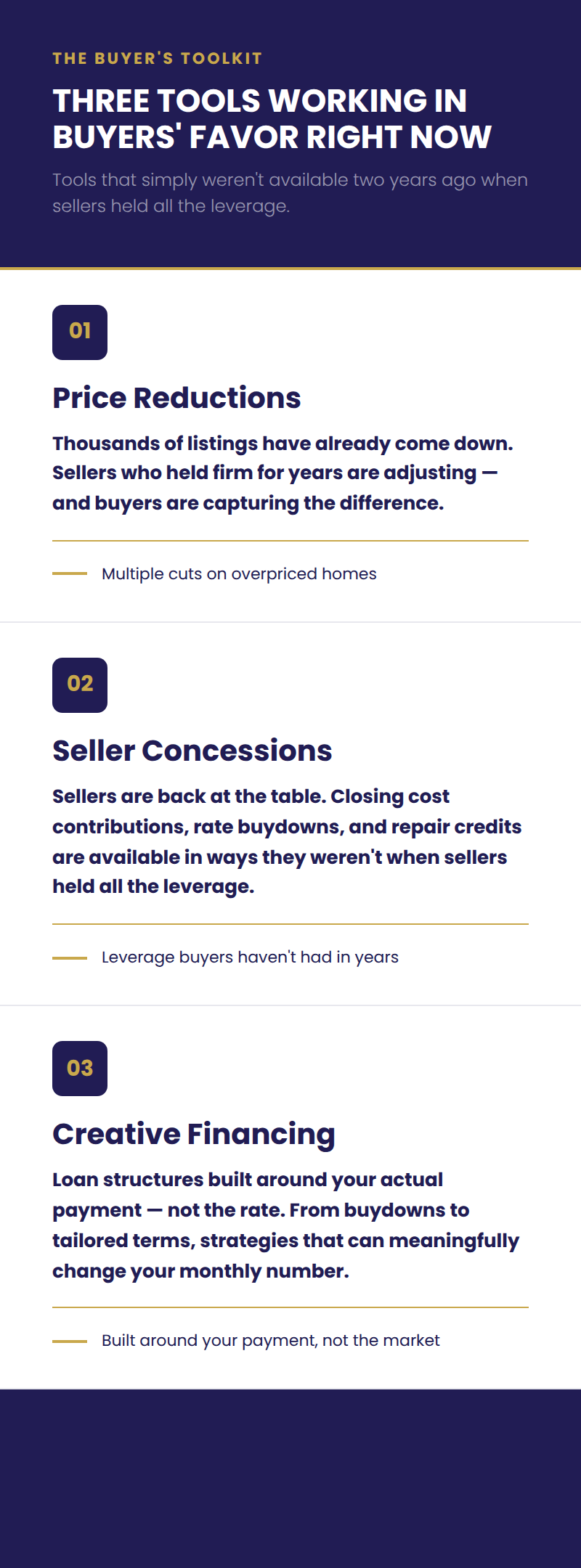

Right now, buyers have tools they didn’t have two years ago when sellers held all the leverage. Seller concessions are back. Creative financing structures are available that can meaningfully change your monthly payment.

Thousands of listings have already come down in price. These aren’t small things — they’re the kind of market conditions that buyers in 2022 would have traded almost anything for.

Phoenix isn’t going anywhere. Jobs are growing, people are still relocating here, and the long-term demand that supports home values remains intact. The question isn’t whether the market will reward patient, strategic buyers. It always has.

The question is whether you’re building a strategy around your actual situation — or waiting for a certainty that isn’t coming. If you’ve been thinking about buying, start with one question: What payment works for your life right now? Everything else can be built from there.